Comments below by Dr Andrew Golding, chief executive of the Pam Golding Property group

South Africa’s residential property market is expected to face renewed pressure this week as the South African Reserve Bank (SARB), as widely anticipated, raised the repo rate by 25 basis points in a pre-emptive move aimed at reinforcing policy credibility as inflation risks rise.

While higher borrowing costs will add to already strained household budgets, the hike is modest and unlikely to derail market activity in South Africa’s resilient residential property market in the short term.

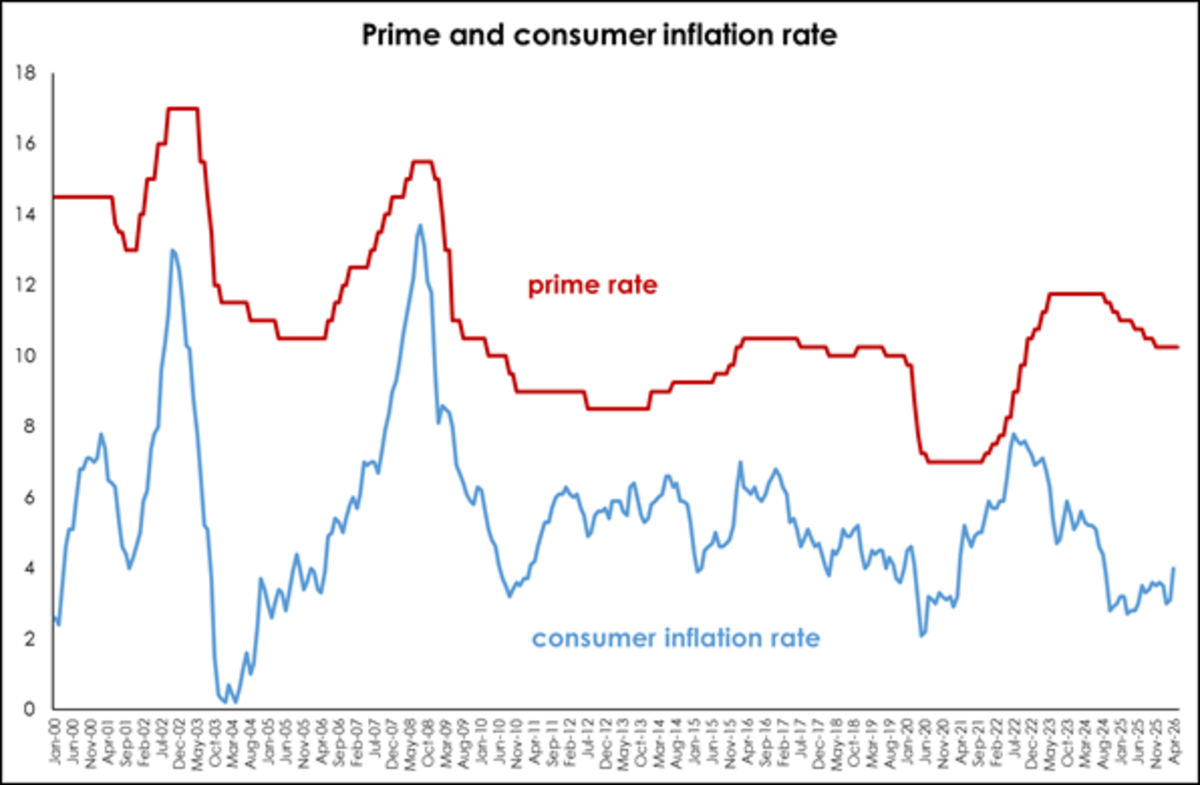

Prime lending rates (now 10.5% vs repo rate of 7%) remain broadly in line with levels seen between 2016 and 2019, making the latest hike more of a moderate adjustment than a major tightening of financial conditions.

Source: SA Reserve Bank & Statistics SA

The increase comes despite a sluggish local economy and mounting pressure on consumers from rising electricity tariffs, fuel prices, municipal rates and water costs.

The SARB’s focus is not on reducing the unavoidable hikes in fuel prices but on protecting longer-term price stability. By acting early, policymakers aim to prevent inflation expectations from drifting higher and to avoid the need for more aggressive action later. A firmer rand, supported by the rate hike, would also help to contain imported inflation, particularly fuel and oil costs.

Markets are currently pricing in a further 25 basis point hike before year-end, although this could change depending on global economic conditions and geopolitical developments. Much will depend on what happens internationally, particularly developments in the Middle East and the stance of major central banks. If global inflation pressures ease, the domestic outlook could improve fairly quickly.

Property market resilience continues

Despite expectations of additional interest rate hikes, banks continue to support the residential property market through increasingly competitive lending conditions.

Banks are working hard to offset deteriorating affordability by offering more zero-deposit home loans and cost-inclusive bonds. Applications for these products are steadily increasing, helping to sustain housing demand.

The real risk would emerge only if banks start questioning the sustainability of household debt and respond by tightening credit, which typically occurs only when consumers are under considerable financial stress. Encouragingly, there is little evidence of the banks taking such action at present.

Higher interest rates are nevertheless expected to place additional pressure on lower- and middle-income households, making affordability an increasingly important consideration for prospective buyers.

Demand shifts toward convenience and smaller homes

The combination of rising transport costs, congestion, and higher living expenses is also expected to reinforce existing lifestyle and housing trends already visible across major metropolitan areas.

There is growing demand for smaller, well-located properties close to workplaces, schools, retail amenities and public transport.

This trend is particularly evident in higher-density nodes such as Claremont (Cape Town), the Cape Town CBD and Rosebank in Johannesburg, where apartment developments offering walkability and easier commuting continue to attract buyers.

Households are becoming smaller, with more people living alone and delaying marriage or children, which continues to support demand for compact homes in convenient locations.

Affordability pressures and traffic congestion were already driving this trend, and prolonged higher fuel costs will likely accelerate it further.

The current environment may also encourage more flexible workplace arrangements, although a full return to widespread work-from-home policies appears unlikely.

Some companies may soften office attendance requirements if commuting costs remain elevated, but many employers remain cautious after encountering resistance when encouraging staff to return to the office post-Covid.

Where remote work flexibility is limited, demand may increasingly shift toward properties located near major transport routes and systems such as the Gautrain and MyCiTi.

All comments above by Dr Andrew Golding, chief executive of the Pam Golding Property group

For further information visit www.pamgolding.co.za